Down Payment Assistance Explained: What and How to Search?

As a loan officer, I hear the same story almost every single week: “I can comfortably afford the monthly mortgage, but saving tens of thousands of dollars for a down payment feels completely out of reach.” If you are feeling stuck in this rent cycle, you are far from alone.

Thankfully, down payment assistance (DPA) programs exist specifically to bridge this gap. In this guide, I will break down exactly how these programs work, who qualifies, and how to find them.

Key Takeaways

- Massive Availability: There are over 2,600 active programs across the United States, providing an average benefit of about $18,000 to eligible buyers.

- Flexible Aid: Assistance comes in various formats, including interest-free grants, forgivable loans, and deferred repayment plans.

- Expanding Limits: More programs are relaxing rules, with over 60% now allowing household income limits above $100,000.

- Smart Searching: Finding these local opportunities is much simpler now using tools like Fannie Mae’s lookup directory and modern AI-powered mortgage guideline assistants.

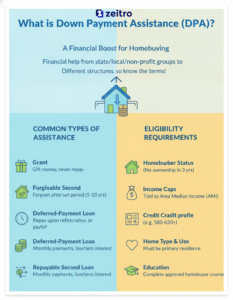

What is Down Payment Assistance (DPA)?

When I explain DPA to my clients, I describe it as a financial boost provided by state housing authorities, local governments, or non-profit groups to help cover your upfront homebuying costs. The money can be structured in a few different ways, so it is important to know what you are signing up for.

The most common types of assistance include:

- Grants: This is essentially gift money that you never have to repay, which is the most sought-after option.

- Forgivable Second Mortgages: These loans are forgiven after you live in the home for a set period, such as five or ten years.

- Deferred-Payment Loans: You do not make payments on this second loan until you sell the home, refinance, or pay off your primary mortgage.

- Repayable Second Loans: You pay this back monthly alongside your main mortgage, usually at a low or zero-percent interest rate.

Eligibility Requirements of Down Payment Assistance

In my years in the mortgage industry, I have learned that no two DPA programs are identical. While there is no single rulebook, most programs use a combination of standard criteria to evaluate applicants. Understanding these requirements beforehand will save you a lot of frustration during your search.

Here are the primary eligibility boxes you will need to tick:

- Homebuyer Status: Most programs target first-time buyers, defined as anyone who has not owned a primary residence in the past three years.

- Income Caps: These are tied to your local Area Median Income (AMI). Interestingly, many programs have raised these limits lately to accommodate rising home prices.

- Credit Qualifications: You typically still need a decent credit profile, often requiring a score of at least 580 to 620 depending on the program.

- Home Type and Use: The property must be your primary residence. Some programs also restrict the home’s purchase price.

- Education: You will almost always need to complete a quick, approved homebuyer education course to understand the responsibilities of homeownership.

How to Find Down Payment Assistance Programs?

Years ago, finding these programs meant calling local housing agencies, digging through outdated state websites, and hoping you did not miss a local city grant. Today, technology has made the search incredibly simple. I recommend focusing on two highly effective resources to find the right program for your scenario.

1. Fannie Mae’s Down Payment Assistance Tool

Fannie Mae offers a direct, consumer-friendly search portal. By entering some basic details about your income, location, and household size, you can quickly generate a list of verified programs that align with your background. It is an excellent, official starting point for any borrower.

2. Zeitro Strata AI

If you want to take your search to a much deeper level—or if you are a mortgage professional trying to verify complex rules—I highly recommend Zeitro Strata AI and its DPA Finder.

Instead of reading through dry, hundred-page PDF manuals, this AI-powered assistant allows you to ask natural questions to find state-specific programs and instantly check the local Area Median Income (AMI) limits. It cross-checks guidelines from over 100 investors (such as AD Mortgage, CMG Financial, and Freedom Mortgage), pulling from a massive database of over 1,000 guidelines.

Whether you need to know if a specific program works with an FHA loan or how a non-QM asset utilization program fits your situation, it cuts manual research from half an hour down to seconds. It even gives you citation-backed answers so you can verify the exact source of the guidelines.

FAQs About Down Payment Assistance

Q1. What does down payment assistance help with?

While the name implies it is only for your down payment, most DPA programs are much more flexible. I often use these programs to help my clients cover their closing costs, which can easily add another 2% to 5% to the home’s purchase price. Depending on the specific program’s rules, the funds can also go toward prepaid expenses like homeowner’s insurance, property taxes, or even buying down your mortgage interest rate to lower your ongoing monthly payments.

Q2. What are the risks of down payment assistance?

No financial program is entirely free of trade-offs. The main risk with DPA is that some programs carry higher interest rates on the first mortgage to offset the assistance costs. Additionally, if you receive a forgivable second loan and need to relocate or sell the home earlier than expected, you might have to pay back a prorated portion of that assistance immediately. It also adds a second lien to your property, which can make a future refinance slightly more complex.

Q3. Can I combine multiple down payment assistance programs?

Yes, in many cases you can. We call this “stacking” or “layering” assistance. For example, you might combine a state-level grant with a local city-funded second mortgage. However, every program has strict rules about where your other funds can come from. Your primary lender must also approve the arrangement. It is vital to have your loan officer cross-check the guidelines of each program to make sure they are compatible before you write an offer on a house.

Q4. How does Area Median Income (AMI) impact my DPA eligibility?

Because DPA programs are designed to help low-to-moderate-income families, they use the Area Median Income (AMI) as a benchmark. If a program limits eligibility to 80% of the local AMI, and the median income in your county is $100,000, your household cannot earn more than $80,000 to qualify. Since these limits vary wildly by zip code and family size, keeping up with them manually is tough. This is where tools like Zeitro Strata AI are incredibly helpful for a quick, precise lookup.

Q5. Can self-employed individuals apply for DPA, and how is income verified?

Absolutely. Being self-employed does not disqualify you from receiving down payment help. However, verifying your income is definitely more complex. Instead of a simple W-2, you will need to provide tax returns, profit and loss statements, or bank statements. If you are applying for non-QM loans, finding a DPA program that aligns with alternative income documentation can be tricky. Using an AI tool to instantly search investor guidelines and automatically calculate self-employed income qualifications can make this process a lot smoother.

Conclusion

The journey to homeownership does not have to be delayed for years while you struggle to save every penny for a down payment. With thousands of programs available across the country offering substantial financial help, the opportunity is likely closer than you think.

Finding the right program just requires the right approach. Start with Fannie Mae’s official calculator, and then useZeitroto quickly search local programs, check AMI, and double-check lender guidelines. Whether you are a first-time homebuyer or a real estate professional, leveraging these digital tools can turn a stressful, weeks-long search into a clear and manageable path forward.

Leave a Reply